The companies and business groups that produce and market software generally meet in most cases certain characteristics from a financial standpoint. And the production / sale of software is almost the end of economies of scale imaginable case. Most of the costs relate to initial development investments, but once developed the product, the marginal cost of selling one more unit is virtually zero. If you have 20,000 customers, the cost of providing customer 20,001 software is null because the software is developed and there is no physical limit its distribution.

However, getting a good product or just getting customers is extremely complicated. Software development has some similarities to scientific research base, one tries several times but the end result is never assured. Getting customers is not easy as there are complex products, often affecting the most basic operation of a business, and it’s not easy to convince / explain the benefits derived therefrom. It is obvious that a database generates cost savings but is almost impossible to quantify ex ante. Therefore, the two major investments of these companies are R & D (Research and Development) and commercial sales or expenses (Sales and Marketing). And as shown by the financial reports of such companies.

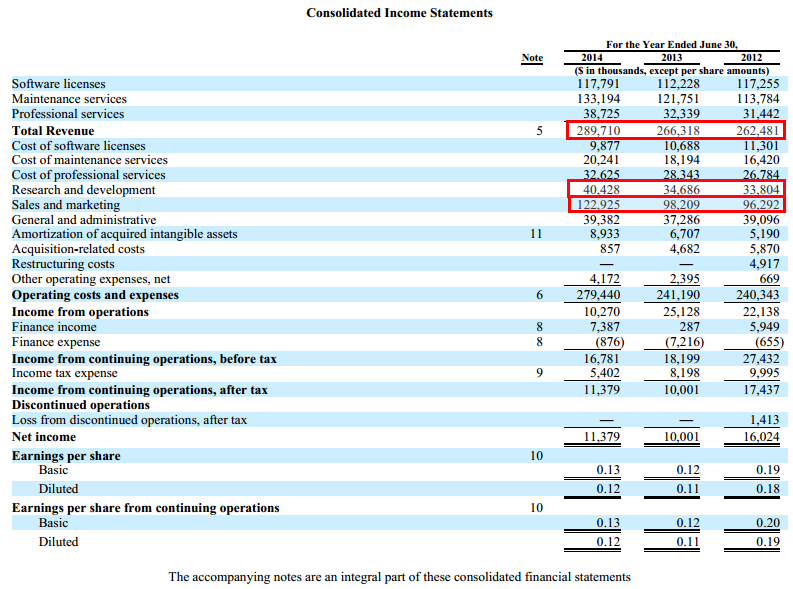

Let’s look at the income of some of these companies. First, a well-known to followers of this blog. Kofax

Kofax spent 13.95% of its sales to R & D investments excluding acquisitions, in which we might take as a reference their expenses Amortization of Intangible Assets (Amortization of acquired intangible assets). More important is currently spending in Sales and Marketing (Sales and Marketing), whose main objective is to achieve new customers. Keep in mind that when Kofax manages a customer, it tends to remain so for many years. The hard part here is not getting new customers but maintain.

Noting the income of this company, one immediately notices that the benefit is a secondary data. His most important investments are not counted as such but as expenses are amortized at the time they are applied except for acquisitions. And should be treated as investments and not expenses as business expense associated largely with clients to remain so for many years. An important part of spending on sales and marketing and R & D is not necessary for the current operation of the company, but for future growth.

Once understood, the most relevant of a company of this profile are sales. Software companies generally have spectacular gross margins between 70 and 80%, hence is easy to make a profit if one forgets to grow the company. If Kofax had maintained their spending on Marketing and Sales frozen since 2012, operating profit would now 36.9 million, more than triple the current. We see that playing with discretionary spending decisions the official number of benefits trips or falls, without the business situation has changed significantly. Therefore, the main conclusion is that in a software company what matters are the sales and growth.

In fact, they understand the market. Then I show the income statements of companies with the same profile, spectacular gross margins, huge expenses in Sales and Marketing with R & D. Some of them have even benefits and yet gigantic valuations obtained bag.

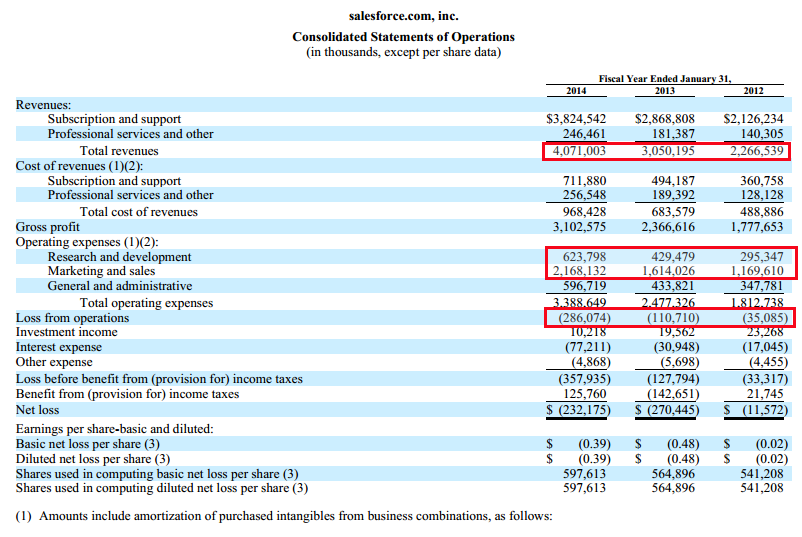

A competitor Oracle is growing strongly in recent years is Salesforce and products based database in the cloud

Spending in Sales and Marketing of total revenues was 53.25% in 2014. The R & D for the same period was the 15.30%. As we see, this company invests more resources than they get and that is why you get a loss in operating income. And despite that the market valued at 34.75 billion dollars, 8.53 times sales

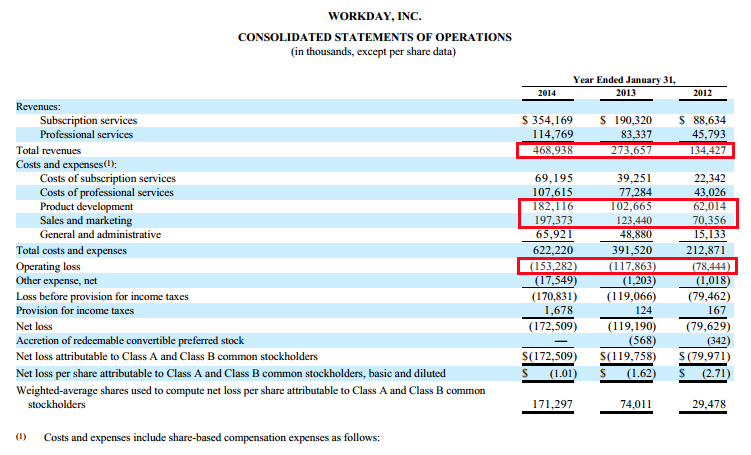

Another competitor of Salesforce and Oracle is Workday, a company that has spectacular growth in sales.

Again, investment in sales and marketing is very high, 42% of sales in 2014. As Salesforce shows a loss in operating income. And as in the case of Salesforce market valuation may surprise some: 15.26 billion, 32.54 times its sales.

Other companies with the same structure are Tableau Software, Red Hat, Akamai Technologies, Service Now, Automatic Data Processing or EMC Corporation. If we compare these 6 companies and take some data we realize that there is a clear relationship between multiple sales discounted by the market and its growth rate current sales. Multiple sales is simply the result of dividing the market capitalization between current sales of a company. In this case we have adjusted by subtracting the net cash to its capitalization. The following table shows the data we will use in the following graph:

Is there any relationship between sales growth and multiple sales discounted by the market? It seems so:

The linear regression leave a correlation coefficient of 93.2% for a sample of nine companies.

In short, it seems that the market is fixed in sales and operating solely quantitative growth. It is not surprising, since as we have seen the benefits in these businesses are quite coarse due to the distortion of classifying investments and costs and economies of scale of these companies, if still growing skyrocket your profits in the future.

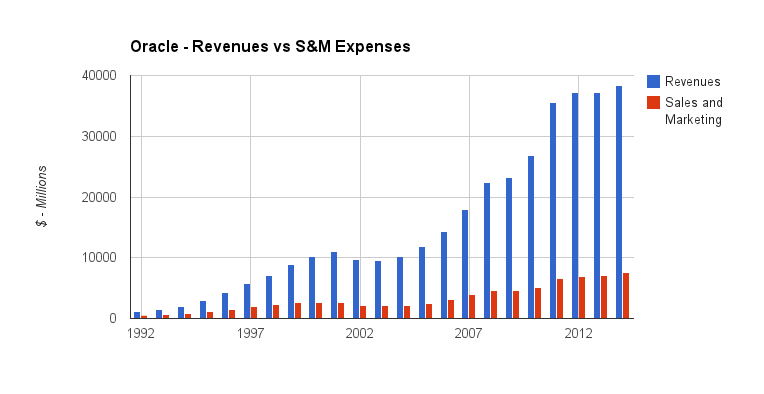

However, it seems dangerous to extrapolate growth rates of 70-80% indefinitely. To get an idea we can take the example of Oracle as fully successful history of growth in the software industry. In the past 22 years, the biggest winner of the software industry achieved a growth of 19% annualized. Extrapolate compound rates above 19% would seem naive, whether superiors are achieved in a few years. Keep in mind that there is greater competition, especially in the case of databases, and must incorporate the scenario where not end up being the winners of this race to the bottom.

Recently I was seeing Peter Thiel conference in which he explains his vision of success stories in the world of technological innovation, which emphasizes the important role of discounting growth from a financial standpoint idea.

Notes that are not as important current growth numbers as its durability. The most important idea of your conference is ideal for a winning technology business is totally dominate a niche and grow, rather than fight for a bigger market to reach more customers faster. In the first case, although the initial growth is less, the durability of that growth is well above the second case, which will eventually be fierce competition (“start big and shrink”).

In that sense, I think too much growth for companies like Workday or Tableau discounted. In fact, they are competing with each other, if you also add a giant like Oracle. Typically existing customers remain attached to their suppliers for many years, but what the market discounts are many new customers. It is possible that all the time end up being the next Oracle. Viewing Oracle trajectory shows how the growth was not linear, but accelerates and decelerates, even reaching back in 2000:

What if circumstantially these growth rates are drastically reduced for a couple of years? Well, following the current logic of the market would be hit hardest Workday, Tableau and Service Now. Workday traded worth 15.26 billion which represents a multiple of sales discounting his box of 28. To see which would be a multiple scenario on profits could reference the Oracle net margin is slightly higher than 25% of sales, then the multiple about hypothetical benefits would be 4 times multiple on current sales:

Multiple on hypothetical benefits = 28 * 4 = 112

I am seems excessive given that we are using rather optimistic assumptions. It may not achieve this margin, or get one of the big winners. Given that it is not impossible scenario in which growth slows dramatically, we have a very optimistic assessment by market Workday.

However, in the case of Kofax although its 9% annual growth will slow, considering a net margin of 10% (not as optimistic as before), would now have a multiple of benefits:

Multiple sobe hypothetical benefits = 1.98 * 6.6 = 13.06

Of course it is not as optimistic as the previous valuation. What is important is the durability of the growth of these companies, not so much what its current growth. Are these companies leaders in their product? Do you have an insurmountable niche from which grow gradually? These are the questions that investors should be. In exchange predominates quantitative in the present, while in the future commanding the qualitative aspects to be reflected in figures that may have nothing to do with the current

Related Content.

No comments:

Post a Comment